by NFS | Jan 12, 2012 | Archives

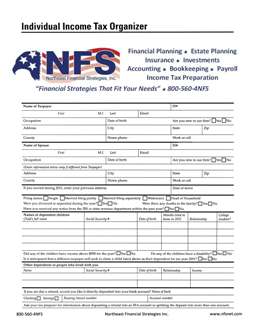

January is a good time to review your finances for the previous year and start organizing the documents and information you’ll need for preparing your tax return. One technique I’ve been using with some of my clients is to make a list of various types of income and tax-deductible expenses you had for 2011.

When your tax documents arrive in the mail, you can check them off your list. In this way you’ll know when all your documents have arrived, and then you’ll be ready to file your tax return.

This technique is especially useful if you have lots of documents, as it can help both you and me, your tax preparer, ensure that all items have been accounted for.

Now each person’s checklist will look a little bit different, since we all have slightly different financial situations.

Here’s one sample checklist for married homeowners:

- W-2 for the husband

- W-2 for the wife

- 1099-INT for savings account

- 1098 for mortgage interest paid

- Property tax statements

- Receipts for any energy-efficient home improvements

Once you develop your checklist, you’ll be able to tell when you have all your documents ready, and you’ll be able to cross-check your progress in your tax software or be able to cross-check your tax preparer’s work.

Your checklist can be as detailed or as simple as you need it to be. If you want to avoid having to create your own checklist, you can download a copy of my organizer here.

by NFS | Jan 10, 2012 | Archives

WASHINGTON — The Internal Revenue Service today reopened the offshore voluntary disclosure program to help people hiding offshore accounts get current with their taxes and announced the collection of more than $4.4 billion so far from the two previous international programs.

The IRS reopened the Offshore Voluntary Disclosure Program (OVDP) following continued strong interest from taxpayers and tax practitioners after the closure of the 2011 and 2009 programs. The third offshore program comes as the IRS continues working on a wide range of

international tax issues and follows ongoing efforts with the Justice Department to pursue criminal prosecution of international tax evasion. This program will be open for an indefinite period until otherwise announced.

“Our focus on offshore tax evasion continues to produce strong, substantial results for the nation’s taxpayers,” said IRS Commissioner Doug Shulman. “We have billions of dollars in hand from our previous efforts, and we have more people wanting to come in and get right with the government. This new program makes good sense for taxpayers still hiding assets overseas and for the nation’s tax system.”

The program is similar to the 2011 program in many ways, but with a few key differences. Unlike last year, there is no set deadline for people to apply. However, the terms of the program could change at any time going forward. For example, the IRS may increase penalties in the program for all or some taxpayers or defined classes of taxpayers – or decide to end the program entirely at any point.

“As we’ve said all along, people need to come in and get right with us before we find you,” Shulman said. “We are following more leads and the risk for people who do not come in continues to increase.”

The third offshore effort comes as Shulman also announced today the IRS has collected $3.4 billion so far from people who participated in the 2009 offshore program, reflecting closures of about 95 percent of the cases from the 2009 program. On top of that, the IRS has collected an additional $1 billion from up front payments required under the 2011 program. That number will grow as the IRS processes the 2011 cases.

In all, the IRS has seen 33,000 voluntary disclosures from the 2009 and 2011 offshore initiatives. Since the 2011 program closed last September, hundreds of taxpayers have come forward to make voluntary disclosures. Those who have come in since the 2011 program closed last year will be able to be treated under the provisions of the new OVDP program.

The overall penalty structure for the new program is the same for 2011, except for taxpayers in the highest penalty category.

For the new program, the penalty framework requires individuals to pay a penalty of 27.5 percent of the highest aggregate balance in foreign bank accounts/entities or value of foreign assets during the eight full tax years prior to the disclosure. That is up from 25 percent in the 2011 program. Some taxpayers will be eligible for 5 or 12.5 percent penalties; these remain the same in the new program as in 2011.

Participants must file all original and amended tax returns and include payment for back-taxes and interest for up to eight years as well as paying accuracy-related and/or delinquency penalties.

Participants face a 27.5 percent penalty, but taxpayers in limited situations can qualify for a 5 percent penalty. Smaller offshore accounts will face a 12.5 percent penalty. People whose offshore accounts or assets did not surpass $75,000 in any calendar year covered by the new OVDP will qualify for this lower rate. As under the prior programs, taxpayers who feel that the penalty is disproportionate may opt instead to be examined.

The IRS recognizes that its success in offshore enforcement and in the disclosure programs has raised awareness related to tax filing obligations. This includes awareness by dual citizens and others who may be delinquent in filing, but owe no U.S. tax. The IRS is currently developing procedures by which these taxpayers may come into compliance with U.S. tax law. The IRS is also committed to educating all taxpayers so that they understand their U.S. tax responsibilities.

More details will be available within the next month on IRS.gov. In addition, the IRS will be updating key Frequently Asked Questions and providing additional specifics on the offshore program.

IR-2012-5

by NFS | Jan 9, 2012 | Archives

Q: I participate in a company 401(k) and have accumulated a large sum over the years. I would like to convert this money into either a Roth IRA or a Roth 401(k), neither of which is offered by my company for the employees. Is there any way (short of hardship or borrowing) to access this money?

A: If your company does not offer a Roth 401(k) plan option, you cannot

use a Roth 401(k). It is that simple. Your 401(k) plan document or summary plan description will state under what conditions you can withdraw from the plan. If you are eligible to take a withdrawal (watch out for adverse consequences), you can convert to a Roth IRA. A hardship withdrawal will not be eligible for conversion to a Roth IRA or for rollover to an IRA. You will, of course, pay income tax on the pretax dollars at the time of the conversion. It is always preferable to pay any income tax due on the conversion with outside money rather than using the IRA funds.

by NFS | Jan 6, 2012 | Archives

WASHINGTON — The Internal Revenue Service today released new proposed guidelines designed to provide relief to more innocent spouses requesting equitable relief from income tax liability.

A Notice proposing a new revenue procedure, posted today on IRS.gov, revises the threshold requirements for requesting equitable relief and revises the factors used by the IRS in evaluating these requests. The factors have been revised to ensure that requests for innocent spouse relief are granted under section 6015(f) when the facts and circumstances warrant and that, when appropriate, requests are granted in the initial stage of the administrative

process. The new guidelines are available immediately and will remain available until the finalized revenue procedure is published. The IRS will immediately begin using these new guidelines when evaluating equitable relief requests.

“

The IRS is significantly changing the way we determine innocent spouse relief,” said IRS Commissioner Doug Shulman. “These improvements should dramatically enhance our process to make it fairer for victimized taxpayers facing difficult situations.”

This is the second major change made to the innocent spouse program. In July, the IRS extended help to more innocent spouses by eliminating the two-year time limit that previously applied to requests seeking equitable relief.

The IRS invites public comment on the proposed revenue procedure. There are three ways to submit comments.

- E-mail to: Notice.Comments@irscounsel.treas.gov. Include “Notice 2012-8” in the subject line.

- Mail to: Internal Revenue Service, CC:PA:LPD:PR (Notice 2012-8), Room 5203, P.O. Box 7604, Ben Franklin Station, Washington, DC 20044.

- Hand deliver to: CC:PA:LPD:PR (Notice 2012-8), Courier’s Desk, Internal Revenue Service, 1111 Constitution Avenue NW, Washington, DC, between 8 a.m. and 4 p.m., Monday through Friday.

The deadline is Feb. 21, 2012.

IR-2012-3