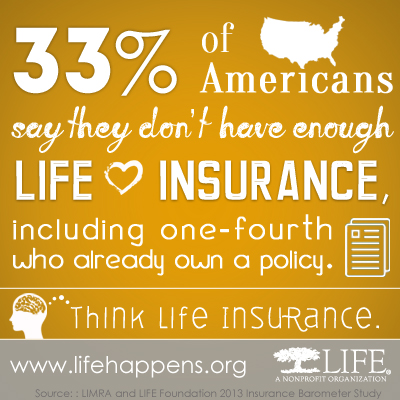

by NFS | Sep 23, 2016 | Archives

No one knows what the future holds. Hopefully, only good things are in store for you.

But realistically, bad things will happen too.

Even if you don’t consider yourself a cautious person, you take little steps every day to improve the odds that good things will happen and guard against the possibility of bad things happening.

You wear seat belts.

You lock your doors when you leave home.

You try to eat well and exercise.

In other words, you may not be able to control the future, but you can stand up to it. You don’t have to get wet when it rains. You can carry an umbrella.

True, it’s easy to take these little steps. The bigger steps, though, can require contemplating some pretty unpleasant things.

What would happen to your family if you became ill or injured and couldn’t work? Or, worse yet, if you died? Or if your spouse died?

Standing up to the future means making sure you and your family can carry on, even in the face of a disaster. That’s where life insurance and other forms of insurance come in.

Life insurance won’t guarantee you’ll never face a tragic situation, just as wearing a seat belt won’t keep you from crashing your car. But it will provide your family with financial protection. And whatever hopes and dreams you have for your loved ones can still be realized, even if the worst were to happen.

That’s why we say LIFE Happens. It really does. No matter what the future throws at you. September is Life Insurance Awareness Month and we here at Northeast Financial Strategies are offering Complimentary Life Insurance Reviews – contact us for your appointment now!

Wrentham, Norfolk, Plainville, Franklin, Walpole, Wrentham insurance, insurance, life insurance, best place for insurance in wrentham, best insurance agency in wrentham, wrentham, LIFE, life insurance awareness month

by NFS | Sep 22, 2016 | Archives

Income tax may be the last thing on your mind after a divorce or separation. However, these events can have a big impact on your taxes. Alimony and a name change are just a few items you may need to consider. Here are some key tax tips to keep in mind if you get divorced or separated.

- Child Support. If you pay child support, you can’t deduct it on your tax return. If you receive child support, the amount you receive is not taxable.

- Alimony Paid. If you make payments under a divorce or separate maintenance decree or written separation agreement you may be able to deduct them as alimony. This applies only if the payments qualify as alimony for federal tax purposes. If the decree or agreement does not require the payments, they do not qualify as alimony.

- Alimony Received. If you get alimony from your spouse or former spouse, it is taxable in the year you get it. Alimony is not subject to tax withholding so you may need to increase the tax you pay during the year to avoid a penalty. To do this, you can make estimated tax payments or increase the amount of tax withheld from your wages.

- Spousal IRA. If you get a final decree of divorce or separate maintenance by the end of your tax year, you can’t deduct contributions you make to your former spouse’s traditional IRA. You may be able to deduct contributions you make to your own traditional IRA.

- Name Changes. If you change your name after your divorce, notify the Social Security Administration of the change. File Form SS-5, Application for a Social Security Card. You can get the form on SSA.gov or call 800-772-1213 to order it. The name on your tax return must match SSA records. A name mismatch can delay your refund.

Health Care Law Considerations

- Special Marketplace Enrollment Period. If you lose your health insurance coverage due to divorce, you are still required to have coverage for every month of the year for yourself and the dependents you can claim on your tax return. Losing coverage through a divorce is considered a qualifying life event that allows you to enroll in health coverage through the Health Insurance Marketplace during a Special Enrollment Period.

- Changes in Circumstances. If you purchase health insurance coverage through the Health Insurance Marketplace you may get advance payments of the premium tax credit in 2016. If you do, you should report changes in circumstances to your Marketplace throughout the year. Changes to report include a change in marital status, a name change and a change in your income or family size. By reporting changes, you will help make sure that you get the proper type and amount of financial assistance. This will also help you avoid getting too much or too little credit in advance.

- Shared Policy Allocation. If you divorced or are legally separated during the tax year and are enrolled in the same qualified health plan, you and your former spouse must allocate policy amounts on your separate tax returns to figure your premium tax credit and reconcile any advance payments made on your behalf. Publication 974, Premium Tax Credit, has more information about the Shared Policy Allocation.

We are here to help. If you would like your FREE Life Guide “Dealing with Divorce” provided by NFS, please request ithere. Otherwise, please contact our office for help.

Wrentham, Norfolk, Plainville, Franklin, Walpole, income tax, tax calculator, hr, irs forms, Jackson Hewitt, tax, tax act, tax return, tax brackets, income tax return, tax refund, taxes, accountant, h&r, tax return calculator, tax forms, free tax filing, federal income tax, federal tax forms, federal tax return, tax online, tax returns, online tax return, irs e file, tax return status, file taxes online, tax preparation, income tax return online, instant tax services, accountants, income tax filing, income tax forms, federal tax, estimate tax return, taxes online, online tax filing, tax services, federal taxes, what is income tax, tax filing, tax questions, online tax, e filing income tax, irs free file, free tax preparation, filing taxes, file taxes, state taxes, tax accountant, h and r, tax planning, free tax return, free federal tax filing, online taxes, free state tax filing, free online tax filing, federal income tax forms, tax help, free tax, how to file taxes, tax preparer, tax consultant, free taxes, income tax returns, complete tax, federal tax forms, free taxes online, income taxes, income tax return efiling, free efile, h&r, tax advisor, tax advice, best place to do taxes in wrentham, wrentham tax, wrentham tax planner, wrentham tax prep, wrentham income, wrentham income tax, wrentham accountant, wrentham accounting

by NFS | Sep 21, 2016 | Archives

So, why do you need life insurance?

What often comes to mind when thinking about life insurance is that you can use it to pay final expenses. You’ve seen the commercials: Funeral expenses, burial costs and medical bills can add up to a hefty amount. The last thing you want is for your loved ones to shoulder this extra burden. Life insurance can be used to plan for these final expenses. Permanent life insurance is available in various amounts, so you can pick a death benefit that meets your needs.

But there are other considerations to keep in mind. You can use life insurance …

As mortgage protection. Whether you live by yourself, with a spouse or significant other, you may want to buy life insurance as mortgage protection. Think about it: You don’t want the person you live with to be homeless if you die unexpectedly, do you? Term life insurance can be used to pay off an outstanding mortgage balance. Just select a term that matches the length of your mortgage payment period. Some companies even offer decreasing term insurance, which means the death benefit decreases along with your mortgage balance.

For income replacement. You and your significant other may have planned for a future based on two incomes, but what if one of you passes away unexpectedly? Life insurance can be used to replace the lost income so the survivor can maintain the same standard of living.

For college funding. Yeah, I know. You don’t have kids, so this one only applies if you do or if you have grandchildren you want to help. Have you seen the tuition rates lately? Life insurance can help fund a college education. If you die, the death benefit may be invested and potentially grow to the needed amount by the time your children or grandchildren reach college age. If you have permanent policies, the cash value may be used to help fund tuition costs. Feel better knowing that you helped prepare for their future—even if you are not there to see it.

There are also a few provisions—additional benefits, if you will—that you may not be aware of.

Probate protection. If the beneficiary of a life insurance policy is a named person and not your estate, the death benefit is free from probate costs.

Incontestability. After the policy has been in force for two years, it becomes incontestable, meaning that the policy cannot be revoked, unless it was fraudulently obtained.

Free from the claims of creditors. In many states, the cash values of the life insurance policy are free from the claims of creditors if the policy is personally owned.

So, are you starting to see the need for life insurance? You will call me right now, right? The number is 800-560-4637 x14. Don’t put it off! Remember, the younger you are when you get insurance, the lower the cost and the easier it is to get approved.

Wrentham, Norfolk, Plainville, Franklin, Walpole, Wrentham insurance, insurance, life insurance, best place for insurance in wrentham, best insurance agency in wrentham, wrentham, LIFE, life insurance awareness month

by NFS | Sep 21, 2016 | Archives

Now, more than ever, is a great time to be a first time home buyer. Housing costs are low, interest rates are at a record low, and you don’t own a home that you have to worry about selling and most likely lose a profit. However, just because it is an ideal time to make that next step, you need to ensure that buying a home is the right choice for you and your current situation.

Buying a home can be fun, exciting, liberating, and a great investment, but it comes with great responsibility, is labor intensive, and a large financial commitment. Once a purchase is made, you are responsible for anything that goes wrong in the house. A new roof, plumbing, new appliances, cutting the lawn, and snow removal now lay in your hands, not a landlord’s.

A few steps to take to figure out if you are ready to be a first time home buyer include:

- Check selling prices in the area you want to live. This will give you some good insight as to how much you will have to pay for the size house that you will need to accommodate you and your lifestyle. Zillow is a great site to see for how much homes in the area have recently sold.

- See how much you can afford. A great tool to use is a mortgage calculator. This allows you to enter the price of the home, the interest rate, the loan term, as well as the property taxes. This will give you a good idea as to how much your monthly housing expenses will be and if it is something you can or cannot afford.

- Get an idea as to how much you will pay in closing costs. This area gets confusing for most. You will see a lot of banks advertise: “No points, no closing costs.” If this is the case, you are paying a slightly higher rate, so that the loan officer gets paid more, so that he or she can use that extra money to pay your closing costs. If you don’t want to pay a chunk of money out of pocket, this may be a good option for you. Otherwise, you can choose to receive the lowest interest rate possible and pay the closing costs out of pocket. The fees that are included in closing costs are: Origination fees charged by the lender, title and settlement fees, taxes and prepaid items such as homeowner’s insurance or homeowner’s association fees.

- Look at your budget. Fannie Mae recommends that buyers spend no more than 28% of their income on housing costs.

- Pick up the phone. Make some calls to your local banks and see who is offering the lowest interest rate. Most will be in the same range, but a few points can make a big difference. Ask questions.

- Make sure your credit is in good standing. One of the largest factors of getting a good interest rate is having good credit. The better the credit score, the lower the rate. The worse your credit score is the higher rate you will receive. In some cases if your credit is so bad, you won’t qualify for a loan at all.

- Inquire about different loan programs. There are several programs out there now that help you to qualify for a home loan. A few include: Mass Housing, FHA, and Veteran’s loans. These are all great programs if you qualify and may more affordable than a conventional loan.

If you follow these basic guidelines then you should successfully be on your way to being a first time home buyer. Here at Northeast Financial Strategies, Inc., we have seamlessly guided thousands of home owners and business people through the buying and selling process. We work with a great local network of realtors, mortgage advisors, closing attorneys and home inspectors. Check out our Events Page to register for our next First Time Home Buyer Seminar happening tonight Wednesday 09/21/2016. If you have any questions regarding the purchase of your first home or would like us to guide you through, please feel free to contact us at: 800-560-4637.

Wrentham, Norfolk, Plainville, Franklin, Walpole, income tax, tax calculator, hr, irs forms, Jackson Hewitt, tax, tax act, tax return, tax brackets, income tax return, tax refund, taxes, accountant, h&r, tax return calculator, tax forms, free tax filing, federal income tax, federal tax forms, federal tax return, tax online, tax returns, online tax return, irs e file, tax return status, file taxes online, tax preparation, income tax return online, instant tax services, accountants, income tax filing, income tax forms, federal tax, estimate tax return, taxes online, online tax filing, tax services, federal taxes, what is income tax, tax filing, tax questions, online tax, e filing income tax, irs free file, free tax preparation, filing taxes, file taxes, state taxes, tax accountant, h and r, tax planning, free tax return, free federal tax filing, online taxes, free state tax filing, free online tax filing, federal income tax forms, tax help, free tax, how to file taxes, tax preparer, tax consultant, free taxes, income tax returns, complete tax, federal tax forms, free taxes online, income taxes, income tax return efiling, free efile, h&r, tax advisor, tax advice, best place to do taxes in wrentham, wrentham tax, wrentham tax planner, wrentham tax prep, wrentham income, wrentham income tax, wrentham accountant, wrentham accounting