by NFS | Jan 25, 2017 | Archives

WASHINGTON — The Internal Revenue Service said this week that it successfully started accepting and processing 2016 federal individual income tax returns on schedule. More than 153 million returns are expected to be filed this year.

People have until Tuesday, April 18, 2017 to file their 2016 returns and pay any taxes due. The deadline is later this year due to several factors. The usual April 15 deadline falls on Saturday this year, which would normally give taxpayers until at least the following Monday. However, Emancipation Day, a D.C. holiday, is observed on Monday, April 17, giving taxpayers nationwide an additional day to file. By law, D.C. holidays impact tax deadlines for everyone in the same way federal holidays do. Taxpayers requesting an extension will have until Monday, Oct. 16, 2017 to file.

“Following months of hard work, we successfully opened our processing systems today to start this year’s tax season,” said IRS Commissioner John Koskinen. “Getting to this point is a year-round effort for the IRS and the nation’s tax community. The dedicated employees of the IRS look forward to serving taxpayers this filing season, and I want to thank all of the tax and payroll community for their hard work that makes tax time smoother for the nation.”

The IRS expects more than 70 percent of taxpayers to get tax refunds this year. Last year, 111 million refunds were issued, with an average refund of $2,860.

Refund Delays

A law change now requires the IRS to hold refunds on tax returns claiming the Earned Income Tax Credit (EITC) or Additional Child Tax Credit (ACTC) until Feb. 15. Under this change required by the Protecting Americans from Tax Hikes (PATH) Act, the IRS must hold the entire refund — even the portion not associated with the EITC and ACTC. Even though the IRS will begin releasing EITC and ACTC refunds on Feb. 15, many early filers will still not have actual access to their refunds until the week of Feb. 27. The additional delay is due to several factors, including weekends, the Presidents Day holiday and the time banks often need to process direct deposits.

This law change gives the IRS more time to detect and prevent fraud. Beyond the EITC and ACTC refunds and the additional security safeguards, the IRS anticipates issuing more than nine out of 10 refunds in less than 21 days. However, it’s possible a particular return may require additional review and take longer. Taxpayers are reminded that state tax agencies have their own refund processing timeframes that vary, and some states may make additional reviews to ensure their refunds are being issued properly. Even so, taxpayers should file as usual, and tax return preparers should submit returns as they normally do.

Use e-File

The IRS expects more than 80 percent of returns to be filed electronically. Choosing e-file and direct deposit remains the fastest and safest way to file an accurate income tax return and receive a refund.

Protecting Taxpayers from Identity Theft-Related Refund Fraud

The IRS continues to work with state tax authorities and the tax industry to address tax-related identity theft and refund fraud. As part of the Security Summit effort, stronger protections for taxpayers and the nation’s tax system are in effect for the 2017 tax filing season.

The new measures attack tax-related identity theft from multiple sides. Many changes will be invisible to taxpayers but will help the IRS, states and the tax industry provide new protections. New security requirements will better protect tax software accounts and personal information.

Renew ITIN to Avoid Refund Delays

Many Individual Taxpayer Identification Numbers (ITINs) expired on Jan. 1, 2017. This includes any ITIN not used on a tax return at least once in the past three years. Also now expired is any ITIN with middle digits of either 78 or 79 (Example: 9NN-78-NNNN or 9NN-79-NNNN). Affected taxpayers should act soon to avoid refund delays and possible loss of eligibility for some key tax benefits until the ITIN is renewed. An ITIN is used by anyone who has tax-filing or payment obligations under U.S. tax law but is not eligible for a Social Security number.

It can take up to 11 weeks to process a complete and accurate ITIN renewal application. For that reason, the IRS urges anyone with an expired ITIN needing to file a return this tax season to submit their ITIN renewal application soon.

New AGI requirement for e-file

All taxpayers should keep a copy of their tax return. Beginning in 2017, taxpayers using a tax filing software product for the first time may need their Adjusted Gross Income (AGI) amount from their prior-year tax return to verify their identity. Taxpayers can learn more about how to verify their identity and electronically sign tax returns at Validating Your Electronically Filed Tax Return.

Filing Assistance

The IRS reminds taxpayers that a trusted tax professional can provide helpful information about the tax laws. A number of tips about selecting a preparer and information about national tax professional groups are available on IRS.gov.

The IRS urges all taxpayers to make sure they have all their year-end statements in hand before filing. This includes Forms W-2 from employers and Forms 1099 from banks and other payers. Doing so will help avoid refund delays and the need to file an amended return.

Please contact our office for help with all of your tax filing needs.

Wrentham, Norfolk, Plainville, Franklin, Walpole, Foxboro, income tax, tax calculator, hr, irs forms, Jackson Hewitt, tax, tax act, tax return, tax brackets, income tax return, tax refund, taxes, accountant, h&r, tax return calculator, tax forms, free tax filing, federal income tax, federal tax forms, federal tax return, tax online, tax returns, online tax return, irs e file, tax return status, file taxes online, tax preparation, income tax return online, instant tax services, accountants, income tax filing, income tax forms, federal tax, estimate tax return, taxes online, online tax filing, tax services, federal taxes, what is income tax, tax filing, tax questions, online tax, e filing income tax, irs free file, free tax preparation, filing taxes, file taxes, state taxes, tax accountant, h and r, tax planning, free tax return, free federal tax filing, online taxes, free state tax filing, free online tax filing, federal income tax forms, tax help, free tax, how to file taxes, tax preparer, tax consultant, free taxes, income tax returns, complete tax, federal tax forms, free taxes online, income taxes, income tax return efiling, free efile, h&r, tax advisor, tax advice, best accountant in Wrentham, best financial planner in Wrentham, best place to do taxes in wrentham, wrentham tax, wrentham tax planner, wrentham tax prep, wrentham income, wrentham income tax, wrentham accountant, wrentham accounting,

by NFS | Jan 6, 2017 | Archives

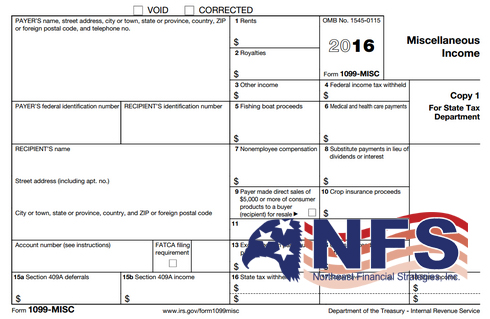

The Internal Revenue Service (IRS) requires you to report certain payments you make as part of your business (including rental properties) to both the payee and IRS. There are new tax law changes regarding 1099-MISC forms that we felt you needed to be made aware of.

If you paid anyone $600 or more during 2016, you and/or your business may need to issue Form 1099-MISC to the individuals or businesses that you paid. This memo will explain your requirements and the penalties for not following the new regulations. We will also explain the costs to engage Northeast Financial Strategies Inc. to prepare these forms for you.

When is a 1099-MISC Required?

You are required to report on Form 1099-MISC when payments are made in the course of your trade or business. This business can be from general business, farming, rentals or any trade or business in which you own with intent to operate for gain or profit.

You must file a Form 1099-MISC, Miscellaneous Income, for each person or entity to who you have paid during the year that is not a Corporation.

- At least $10 in Royalties

- At least $600 in

- Rents

- Services (the dollar amount includes parts and materials)

- Prizes and Awards

- Other Income Payments

- Barter Income

- Medical and Health Care Payments

- Crop Insurance Proceeds

- Cash payments for fish you purchase from anyone engaged in the trade or business of catching fish

- Any fishing boat proceeds

- Gross proceeds of $600 or more paid to an attorney (no exception for corporation)

Generally you do not have to issue a Form 1099-MISC for non-employee compensation paid to a corporation. Payments to corporations are reported only if they are for medical, veterinary, health care, legal or fishing activities.

If the following four conditions are met, you must generally report a payment as non-employee compensation.

*You made the payment to someone who is not your employee (in other words, you didn’t issue them a W-2);

*You made the payment for services or for rent in the course of your trade or business. This also includes payments made by nonprofit organizations;

*You made the payment to an individual, partnership, LLC, estate and in some cases, a corporation; and

*You made total payments to the payee of at least $600 during the calendar year.

Example: If a meat shop business paid a self-employed plumber, Jones Plumbing, $750 for labor and materials to repair and replace floor drains, it would have to issue a Form 1099-MISC to Jones Plumbing. If Jones Plumbing is listed as Jones Plumbing LLC, then a 1099-MISC is still required. However, if the plumber is Jones Plumbing Inc., no 1099 is required. If you are not sure, then it is always better for you to issue the 1099.

What should be included on a Form 1099?

The following information is required by IRS for the processing of the 1099.

- The payee’s full name.

- The social security number or Employer Identification Number.

- The legal address of the individual or business.

- The dollar amount, including labor and material, paid to the payee.

All of this information is obtained from a completed form W-9. We have enclosed one for you that can be photocopied and used. Original W-9’s are not required; photo copies will not be accepted. Our office recommends that you ALWAYS obtain a completed Form W-9 from any new contractor or business BEFORE you issue them a check.

Why should I mess with filing these forms, after all, I am just a very small business? This is a huge hassle!

With the passing of what is termed the PATH Act by Congress, there have been significant changes made to the issue of 1099’s. These are the law changes.

- All 1099’s must be completed and mailed to both the payee and the Internal Revenue Service no later than January 31, 2017.

- The penalty for NOT filing a required 1099 is $100 per form. This means if you have four subcontractors that you paid and you fail to issue 1099’s, your penalty is $400.

- The penalty for Intentional Disregard is $250 per payee. In other words, you received this letter and you decided it was too much of a hassle; you will be fined $1,000 for the same four subcontractors.

- Any expenses on your tax return that required a 1099 to be issued, such as rents and subcontractors, will be disallowed if you fail to file the proper 1099’s.

- There is a check box on all business schedules that ask if you are required to file any 1099’s and if you are, did you do so. If our office prepares your taxes, we will answer this question honestly. Failures on anyone’s part to not answer this question honestly is considered Fraud under the Internal Revenue Code.

Can Northeast Financial Strategies Inc. prepare and file these forms for me?

We are able to prepare all Form 1099’s for you and this year!

In order to complete these forms:

1. Please provide us with a complete list of anyone needing a 1099 form. The following information is required:

a. Name as it appears on the payments you made

b. Address of the payee

c. Social Security number or Employer Identification Number of the payee

d. Total amount you paid to them during 2016

e. Type of payments made, such as payment for services, rents, etc.

2. We will complete 1099 projects in the order they are received at our office.

3. If the package of data you send to us is not complete, we reserve the right to not begin work until the full package is received.

If you have any questions or concerns, please call us at 800-560-4637. Anyone on the NFS team can answer your questions about 1099-MISC filing requirements.

Wrentham, Norfolk, Plainville, Franklin, Walpole, Foxboro, income tax, tax calculator, hr, irs forms, Jackson Hewitt, tax, tax act, tax return, tax brackets, income tax return, tax refund, taxes, accountant, h&r, tax return calculator, tax forms, free tax filing, federal income tax, federal tax forms, federal tax return, tax online, tax returns, online tax return, irs e file, tax return status, file taxes online, tax preparation, income tax return online, instant tax services, accountants, income tax filing, income tax forms, federal tax, estimate tax return, taxes online, online tax filing, tax services, federal taxes, what is income tax, tax filing, tax questions, online tax, e filing income tax, irs free file, free tax preparation, filing taxes, file taxes, state taxes, tax accountant, h and r, tax planning, free tax return, free federal tax filing, online taxes, free state tax filing, free online tax filing, federal income tax forms, tax help, free tax, how to file taxes, tax preparer, tax consultant, free taxes, income tax returns, complete tax, federal tax forms, free taxes online, income taxes, income tax return efiling, free efile, h&r, tax advisor, tax advice, best accountant in Wrentham, best financial planner in Wrentham, best place to do taxes in wrentham, wrentham tax, wrentham tax planner, wrentham tax prep, wrentham income, wrentham income tax, wrentham accountant, wrentham accounting,

by NFS | Jan 3, 2017 | Archives

Instead of using the business portion of the actual expenses of operating a vehicle, IRS permits taxpayers to use a standard mileage rate. The rates have now been released for travel on or after January 1, 2017.

Business rate is 53.5 cents per mile (down from 54 for 2016). The depreciation portion of this rate is 25 cents per mile (up from 24 for 2016).

Charitable rate is 14 cents per mile and is set by Congress therefore will not change until Congress makes such a change.

Medical and moving rate is 17 cents per mile (down from 19 for 2016).

Wrentham, Norfolk, Plainville, Franklin, Walpole, Foxboro, income tax, tax calculator, hr, irs forms, Jackson Hewitt, tax, tax act, tax return, tax brackets, income tax return, tax refund, taxes, accountant, h&r, tax return calculator, tax forms, free tax filing, federal income tax, federal tax forms, federal tax return, tax online, tax returns, online tax return, irs e file, tax return status, file taxes online, tax preparation, income tax return online, instant tax services, accountants, income tax filing, income tax forms, federal tax, estimate tax return, taxes online, online tax filing, tax services, federal taxes, what is income tax, tax filing, tax questions, online tax, e filing income tax, irs free file, free tax preparation, filing taxes, file taxes, state taxes, tax accountant, h and r, tax planning, free tax return, free federal tax filing, online taxes, free state tax filing, free online tax filing, federal income tax forms, tax help, free tax, how to file taxes, tax preparer, tax consultant, free taxes, income tax returns, complete tax, federal tax forms, free taxes online, income taxes, income tax return efiling, free efile, h&r, tax advisor, tax advice, best accountant in Wrentham, best financial planner in Wrentham, best place to do taxes in wrentham, wrentham tax, wrentham tax planner, wrentham tax prep, wrentham income, wrentham income tax, wrentham accountant, wrentham accounting,

by NFS | Jan 1, 2017 | Archives

Here’s to a Happy, Healthy and Prosperous New Year!

“Always bear in mind that your own resolution to succeed is more important than any other.”

-Abraham Lincoln

by NFS | Dec 23, 2016 | Archives

Your friends at Northeast Financial Strategies want you to know how much your loyalty and friendship are appreciated this year and in all years past. At the holiday season, our thoughts turn gratefully to those who have made our success possible. It is in this spirit we say … thank you and best wishes for the holidays and a happy new year.

From all of us here at NFS, THANKS!!

by NFS | Nov 28, 2016 | Archives

When it comes to legal separation or divorce, there are many complex situations to address. A divorcing couple faces many important decisions and issues regarding alimony, child support, and the fair division of property. While most courts and judges will not factor in the impact of taxes on a potential property settlement or cash payments, it is important to realize how the value of assets transferred can be materially affected by the tax implications.

Dependents

One of the most argued points between separating couples regarding taxes is who gets to claim the children as dependents on their tax return, since joint filing is no longer an option. The reason this part of tax law is so important to divorcing parents is that the federal and state exemptions allowed for dependents offer a significant savings to the custodial parent, and there are also substantial child and educational credits that can be taken. The right to claim a child as a dependent from birth through college can be worth over $30,000 in tax savings.

The law states that one parent must be chosen as the head of the household, and that parent may legally claim the dependents on his or her return.

Example: If a couple was divorced or legally separated by December 31 of the last tax year, the law allows the tax exemptions to go to the parent who had physical custody of the children for the greater part of the year (the custodial parent), and that parent would be considered the head of the household. However, if the separation occurs in the last six months of the year and there hasn’t yet been a legal divorce or separation by the year’s end, the exemptions will go to the parent that has been providing the most financial support to the children, regardless of which parent had custody.

A non-custodial parent can only claim the dependents if the custodial parent releases the right to the exemptions and credits. This needs to be done legally by signing tax Form 8332, Release of Claim to Exemption. However, even if the non-custodial parent is not claiming the children, he or she still has the right to deduct things like medical expenses.

Child support payments are not deductible or taxable. Merely labeling payments as child support is not enough — various requirements must be met.

Alimony

Alimony is another controversial area for separated or divorced couples, mostly because the payer of the alimony wants to deduct as much of that expense as possible, while the recipient wants to avoid paying as much tax on that income as he or she can. On a yearly tax return, the recipient of alimony is required to claim that money as taxable income, while the payer can deduct the payment, even if he or she chooses not to itemize.

Because alimony plays such a large part in a divorced couple’s taxes, the government has specifically outlined what can and can not be considered as an alimony expense. The government says that an alimony payment is one that is required by a divorce or separation decree, is paid by cash, check or money order, and is not already designated as child support. The payer and recipient must not be filing a joint return, and the spouses can not be living in the same house. And the payment cannot be part of a non-cash property settlement or be designated to keep up the payer’s property.

There are also complicated recapture rules that may need to be addressed in certain tax situations. When alimony must be recaptured, the payer must report as income part of what was deducted as alimony within the first two payment years.

Property

Many aspects of property settlements are too numerous and detailed to discuss at length, but separating couples should be aware that, when it comes to property distributions, basis should be considered very carefully when negotiating for specific assets.

Example: Let’s say you get the house and the spouse gets the stock. The actual split up and distribution is tax-free. However, let’s say the house was bought last year for $300,000 and has $100,000 of equity. The stock was bought 20 years ago, is also worth $100,000, but was bought for $10,000. Selling the house would generate no tax in this case and you would get to keep the full $100,000 equity. Selling the $100,000 of stock will generate about $25,000 to $30,000 of federal and state taxes, leaving the other spouse with a net of $70,000. While there may be no taxes to pay for several years if both parties plan to hold the assets for some time, the above example still illustrates an inequitable division of assets due to non-consideration of the underlying basis of the properties distributed.

Under a recent tax law, a spouse who acquires a partial interest in a house through a divorce settlement can move out and still exempt up to $250,000 of any taxable gain. This still holds true if he or she has not lived in the home for two of the last five years, the book states. It also applies to the spouse staying in the home. However, the divorce decree must clearly state that the home will be sold later and the proceeds will be split.

Complications and tax traps can also occur when a jointly owned business is transferred to one spouse in connection with a divorce. Professional tax assistance at the earliest stages of divorce are recommended in situations where a closely held business interest is involved.

Retirement

When a couple splits up, the courts have the authority to divide a retirement plan (whether it’s an account or an accrued benefit) between the spouses. If the retirement money is in an IRA account, the individuals need to draw up a written agreement to transfer the IRA balance from one spouse to the other. However, if one spouse is the trustee of a qualified retirement plan, he or she must comply with a Qualified Domestic Relations Order to divide the accrued benefit. Each spouse will then be taxed on the money they receive from this plan, unless it is transferred directly to an IRA, in which case there will be no withholding or income tax liability until the money is withdrawn.

Extreme caution should be exercised when there are company pension and profit-sharing benefits, Keogh plan benefits, and/or IRAs to split up. Unless done appropriately, the split up of these plans will be taxable to the spouse transferring the plan to the other.

Tax Prepayment and Joint Refunds

When a couple prepays taxes by either withholding wages or paying estimated taxes throughout the year, the withholding will be credited to the spouse who earned the underlying income. In community property states, the withholding will be credited equally when spouses each report half of their income. When a joint refund is issued after a couple has separated or divorced, the couple should consult a tax advisor to determine how the refund should be divided. There is a formula that can be used to determine this amount, but it is wisest to use a qualified individual to make sure it is properly applied.

Legal and Other Expenses

To the dismay of most divorcing couples, the massive legal bills most end up paying are not deductible at tax time because they are considered personal nondeductible expenses. On the other hand, if a part of that bill was allocated to tax advice, to securing alimony, or to the protection of business income, those expenses can be deducted when itemizing. However, their total — combined with other miscellaneous itemized deductions — must be greater than 2% of the taxpayer’s adjusted gross income to qualify.

Divorce planning and the related tax implications can completely change the character of the divorcing couple’s negotiations. As many divorce attorneys are not always aware of these tax implications, it is always a good idea to have a qualified tax professional be involved in the dissolution process and planning from the very early stages.

If you are in the process of divorce or are considering divorce or legal separation, please contact the office for a consultation and additional guidance. You can also request a copy of our FREE GUIDE titled “Dealing with Divorce” by clicking here.

|

| FREE GUIDE – “Dealing with Divorce” |

Wrentham, Norfolk, Plainville, Franklin, Walpole, income tax, tax calculator, hr, irs forms, Jackson Hewitt, tax, tax act, tax return, tax brackets, income tax return, tax refund, taxes, accountant, h&r, tax return calculator, tax forms, free tax filing, federal income tax, federal tax forms, federal tax return, tax online, tax returns, online tax return, irs e file, tax return status, file taxes online, tax preparation, income tax return online, instant tax services, accountants, income tax filing, income tax forms, federal tax, estimate tax return, taxes online, online tax filing, tax services, federal taxes, what is income tax, tax filing, tax questions, online tax, e filing income tax, irs free file, free tax preparation, filing taxes, file taxes, state taxes, tax accountant, h and r, tax planning, free tax return, free federal tax filing, online taxes, free state tax filing, free online tax filing, federal income tax forms, tax help, free tax, how to file taxes, tax preparer, tax consultant, free taxes, income tax returns, complete tax, federal tax forms, free taxes online, income taxes, income tax return efiling, free efile, h&r, tax advisor, tax advice, best place to do taxes in wrentham, wrentham tax, wrentham tax planner, wrentham tax prep, wrentham income, wrentham income tax, wrentham accountant, wrentham accounting