by NFS | Sep 29, 2015 | Archives

As we have presented this September, life insurance can do some pretty amazing things for people. It can buy loved ones time to grieve. It can pay off debts and loans, providing surviving family members with the chance to move on with a clean slate. It can keep families in their homes and pre-fund a child’s college education. It can keep a family business in the family. It can provide a stream of income for a family to live on for a period of time. Life insurance can do all of these wonderful things for your family…there’s just one small catch. You need to own life insurance.

There’s a growing crisis of too many Americans not having adequate life insurance protection. According to the industry research group LIMRA, 30 percent of US households have no life insurance whatsoever. Today there are 11 million fewer American households covered by life insurance compared with six years ago. Here’s the bottom line: A majority of families either have no life insurance or not enough, leaving them one accident or terminal illness away from a financial catastrophe for their loved ones.

What if you were suddenly gone and your family had to manage on their own? When was the last time you did the math to make sure your loved ones would be OK financially? Have you checked with your employer to find out what kind of life insurance benefit you have through work and whether you have the option to increase your coverage? When was the last time you had your life insurance needs reviewed by an insurance professional? Northeast Financial Strategies is here to help!

Wrentham, Norfolk, Plainville, Franklin, Walpole, Wrentham insurance, insurance, life insurance, best place for insurance in wrentham, best insurance agency in wrentham, wrentham, LIFE, life insurance awareness month

by NFS | Sep 28, 2015 | Archives

Now, more than ever, is a great time to be a first time home buyer. Housing costs are low, interest rates are at a record low, and you don’t own a home that you have to worry about selling and most likely lose a profit. However, just because it is an ideal time to make that next step, you need to ensure that buying a home is the right choice for you and your current situation.

Now, more than ever, is a great time to be a first time home buyer. Housing costs are low, interest rates are at a record low, and you don’t own a home that you have to worry about selling and most likely lose a profit. However, just because it is an ideal time to make that next step, you need to ensure that buying a home is the right choice for you and your current situation.

Buying a home can be fun, exciting, liberating, and a great investment, but it comes with great responsibility, is labor intensive, and a large financial commitment. Once a purchase is made, you are responsible for anything that goes wrong in the house. A new roof, plumbing, new appliances, cutting the lawn, and snow removal now lay in your hands, not a landlord’s.

A few steps to take to figure out if you are ready to be a first time home buyer include:

- Check selling prices in the area you want to live. This will give you some good insight as to how much you will have to pay for the size house that you will need to accommodate you and your lifestyle. Zillow is a great site to see for how much homes in the area have recently sold.

- See how much you can afford. A great tool to use is a mortgage calculator. This allows you to enter the price of the home, the interest rate, the loan term, as well as the property taxes. This will give you a good idea as to how much your monthly housing expenses will be and if it is something you can or cannot afford.

- Get an idea as to how much you will pay in closing costs. This area gets confusing for most. You will see a lot of banks advertise: “No points, no closing costs.” If this is the case, you are paying a slightly higher rate, so that the loan officer gets paid more, so that he or she can use that extra money to pay your closing costs. If you don’t want to pay a chunk of money out of pocket, this may be a good option for you. Otherwise, you can choose to receive the lowest interest rate possible and pay the closing costs out of pocket. The fees that are included in closing costs are: Origination fees charged by the lender, title and settlement fees, taxes and prepaid items such as homeowner’s insurance or homeowner’s association fees.

- Look at your budget. Fannie Mae recommends that buyers spend no more than 28% of their income on housing costs.

- Pick up the phone. Make some calls to your local banks and see who is offering the lowest interest rate. Most will be in the same range, but a few points can make a big difference. Ask questions.

- Make sure your credit is in good standing. One of the largest factors of getting a good interest rate is having good credit. The better the credit score, the lower the rate. The worse your credit score is the higher rate you will receive. In some cases if your credit is so bad, you won’t qualify for a loan at all.

- Inquire about different loan programs. There are several programs out there now that help you to qualify for a home loan. A few include: Mass Housing, FHA, and Veteran’s loans. These are all great programs if you qualify and may more affordable than a conventional loan.

If you follow these basic guidelines then you should successfully be on your way to being a first time home buyer. Here at Northeast Financial Strategies, Inc., we have seamlessly guided thousands of home owners and business people through the buying and selling process. We work with a great local network of realtors, mortgage advisors, closing attorneys and home inspectors. Check out our Events Page to register for our next First Time Home Buyer Seminar happening tomorrow Wednesday 09/30/2015. If you have any questions regarding the purchase of your first home or would like us to guide you through, please feel free to contact us at: 800-560-4637.

Wrentham, Norfolk, Plainville, Franklin, Walpole, income tax, tax calculator, hr, irs forms, Jackson Hewitt, tax, tax act, tax return, tax brackets, income tax return, tax refund, taxes, accountant, h&r, tax return calculator, tax forms, free tax filing, federal income tax, federal tax forms, federal tax return, tax online, tax returns, online tax return, irs e file, tax return status, file taxes online, tax preparation, income tax return online, instant tax services, accountants, income tax filing, income tax forms, federal tax, estimate tax return, taxes online, online tax filing, tax services, federal taxes, what is income tax, tax filing, tax questions, online tax, e filing income tax, irs free file, free tax preparation, filing taxes, file taxes, state taxes, tax accountant, h and r, tax planning, free tax return, free federal tax filing, online taxes, free state tax filing, free online tax filing, federal income tax forms, tax help, free tax, how to file taxes, tax preparer, tax consultant, free taxes, income tax returns, complete tax, federal tax forms, free taxes online, income taxes, income tax return efiling, free efile, h&r, tax advisor, tax advice, best place to do taxes in wrentham, wrentham tax, wrentham tax planner, wrentham tax prep, wrentham income, wrentham income tax, wrentham accountant, wrentham accounting

by NFS | Sep 27, 2015 | Archives

One of the most important questions you face when changing job is what to do with the money in your 401(k). Making the wrong move could cost you thousands of dollars or more in taxes and lower returns.

Let’s say you put in five years at your current job. For most of those years, you’ve had the company take a set percentage of your pre-tax salary and put it into your 401(k) plan.

Now that you’re leaving, what should you do? The first rule of thumb is to leave it alone because you have 60 days to decide whether to roll it over or leave it in the account.

Resist the temptation to cash out. The worst thing an employee can do when leaving a job is to withdraw the money from their 401(k) plans and put it in his or her bank account. Here’s why:

If you decide to have your distribution paid to you, the plan administrator will withhold 20 percent of your total for federal income taxes, so if you had $100,000 in your account and you wanted to cash it out, you’re already down to $80,000.

Furthermore, if you’re younger than 59 1/2, you’ll face a 10 percent penalty for early withdrawal come tax time. Now you’re down another 10 percent from the original amount of $100,000 to $70,000.

Also, because distributions are taxed as ordinary income, at the end of the year, you’ll have to pay the difference between your tax bracket and the 20 percent already taken out. For example, if you’re in the 33 percent tax bracket, you’ll still owe 13 percent, or $13,000. This lowers the amount of your cash distribution to $57,000.

But that’s not all. You might also have to pay state and local taxes. Between taxes and penalties, you could end up with little over half of what you had saved up, short-changing your retirement savings significantly.

What are the Alternatives?

If your new job offers a retirement plan, then the easiest course of action is to roll your account into the new plan before the 60-day period ends. Referred to as a “rollover” it is relatively painless to do. The 401(k) plan administrator at your previous job should have all of the forms you need.

A word of caution: Many employers require that you work a minimum period of time (e.g. three months) before you can participate in a 401(k). If that is the case, one solution is to keep your money in your former employer’s 401(k) plan until the new one is available. Then you can roll it over into the new plan. Most plans let former employees leave their assets in the old plan for several months.

The best way to roll funds over from an old 401(k) plan to a new one is to use a direct transfer. With the direct transfer, you never receive a check, and you avoid all of the taxes and penalties mentioned above, and your savings will continue to grow tax-deferred until you retire.

60-Day Rollover Period

If you have your former employer make the distribution check out to you, the Internal Revenue Service considers this a cash distribution. The check you get will have 20 percent taken out automatically from your vested amount for federal income tax.

But don’t panic. You have 60 days to roll over the lump sum (including the 20 percent) to your new employer’s plan or into a rollover individual retirement account (IRA). Then you won’t owe the additional taxes or the 10 percent early withdrawal penalty.

Note: If you’re not happy with the fund choices your new employer offers, you might opt for a rollover IRA instead of your company’s plan. You can then choose from hundreds of funds and have more control over your money. But again, to avoid the withholding hassle, use direct rollovers.

Note: Prior to 2015, the IRS allowed a one-per-year limit on rollovers on an IRA-by-IRA basis; however, starting in 2015, the limit will apply to aggregating all of an individual’s IRAs, effectively treating them as if they were a single IRA for the purposes of applying the limit.

Leave It Alone

If your vested account balance in your 401(k) is more than $5,000, you can usually leave it with your former employer’s retirement plan. Your lump sum will keep growing tax-deferred until you retire.

However, if you can’t leave the money in your former employer’s 401(k) and your new job doesn’t have a 401(k), your best bet is a direct rollover into an IRA. The same applies if you’ve decided to go into business for yourself.

Once you turn 59 1/2, you can begin withdrawals from your 401(k) plan or IRA without penalty and your withdrawals are taxed as ordinary income.

You don’t have to start taking withdrawals from your 401(k) unless you retire after age 70 1/2. With an IRA you must begin a schedule of taxable withdrawals based on your life expectancy when you reach 70 1/2, whether you’re working or not.

Don’t hesitate to call if you have any questions about IRA rollovers. We can assist you in the process and find an option that best suits your needs.

Wrentham, Norfolk, Plainville, Franklin, Walpole, income tax, tax calculator, hr, irs forms, Jackson Hewitt, tax, tax act, tax return, tax brackets, income tax return, tax refund, taxes, accountant, h&r, tax return calculator, tax forms, free tax filing, federal income tax, federal tax forms, federal tax return, tax online, tax returns, online tax return, irs e file, tax return status, file taxes online, tax preparation, income tax return online, instant tax services, accountants, income tax filing, income tax forms, federal tax, estimate tax return, taxes online, online tax filing, tax services, federal taxes, what is income tax, tax filing, tax questions, online tax, e filing income tax, irs free file, free tax preparation, filing taxes, file taxes, state taxes, tax accountant, h and r, tax planning, free tax return, free federal tax filing, online taxes, free state tax filing, free online tax filing, federal income tax forms, tax help, free tax, how to file taxes, tax preparer, tax consultant, free taxes, income tax returns, complete tax, federal tax forms, free taxes online, income taxes, income tax return efiling, free efile, h&r, tax advisor, tax advice, best place to do taxes in wrentham, wrentham tax, wrentham tax planner, wrentham tax prep, wrentham income, wrentham income tax, wrentham accountant, wrentham accounting

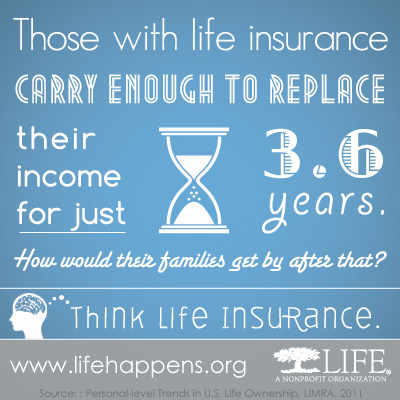

by NFS | Sep 23, 2015 | Archives

Here are some interesting info tidbits on the perceived cost of insurance:

by NFS | Sep 22, 2015 | Archives

Do you want your family to have enough funds to survive without you? Contact our office today to make sure you have enough coverage.

Wrentham, Norfolk, Plainville, Franklin, Walpole, Wrentham insurance, insurance, life insurance, best place for insurance in wrentham, best insurance agency in wrentham, wrentham, LIFE, life insurance awareness month

by NFS | Sep 21, 2015 | Archives

When you start a business, a key to your success is to know your tax obligations. You may not only need to know about income tax rules, but also about payroll tax rules. Here are five IRS tax tips that can help you get your business off to a good start.

When you start a business, a key to your success is to know your tax obligations. You may not only need to know about income tax rules, but also about payroll tax rules. Here are five IRS tax tips that can help you get your business off to a good start.

1. Business Structure. An early choice you need to make is to decide on the type of structure for your business. The most common types are sole proprietor, partnership and corporation. The type of business you choose will determine which tax forms you will file. We can help you to choose the right entity for your situation.

2. Business Taxes. There are four general types of business taxes. They are income tax, self-employment tax, employment tax and excise tax. In most cases, the types of tax your business pays depends on the type of business structure you set up. You may need to make estimated tax payments. If you do, use IRS Direct Pay to pay them. It’s the fast, easy and secure way to pay from your checking or savings account. We can set up all of these tax payment systems for you.

3. Employer Identification Number. You may need to get an EIN for federal tax purposes. Search “do you need an EIN” on IRS.gov to find out if you need this number. If you do need one, you can apply for it online. Getting the EIN is quick, and we can get step you through the process to do so.

4. Accounting Method. An accounting method is a set of rules that you use to determine when to report income and expenses. You must use a consistent method. The two that are most common are the cash and accrual methods. Under the cash method, you normally report income and deduct expenses in the year that you receive or pay them. Under the accrual method, you generally report income and deduct expenses in the year that you earn or incur them. This is true even if you get the income or pay the expense in a later year.

5. Employee Health Care. The Small Business Health Care Tax Credit helps small businesses and tax-exempt organizations pay for health care coverage they offer their employees. A small employer is eligible for the credit if it has fewer than 25 employees who work full-time, or a combination of full-time and part-time. The maximum credit is 50 percent of premiums paid for small business employers and 35 percent of premiums paid for small tax-exempt employers, such as charities. Health Insurance premiums vary across the board depending on the type of plan you look at. We can run the quotes for all options and step you through which plans are the best for you and your small business.

The employer shared responsibility provisions of the Affordable Care Act affect employers employing at least a certain number of employees (generally 50 full-time employees or a combination of full-time and part-time employees). These employers’ are called applicable large employers. ALEs must either offer minimum essential coverage that is “affordable” and that provides “minimum value” to their full-time employees (and their dependents), or potentially make an employer shared responsibility payment to the IRS. The vast majority of employers will fall below the ALE threshold number of employees and, therefore, will not be subject to the employer shared responsibility provisions.

Employers also have information reporting responsibilities regarding minimum essential coverage they offer or provide to their fulltime employees. Employers must send reports to employees and to the IRS on new forms the IRS created for this purpose.

Let us help with all the tax basics of starting a business – contact our office today to get started.

Wrentham, Norfolk, Plainville, Franklin, Walpole, income tax, tax calculator, hr, irs forms, Jackson Hewitt, tax, tax act, tax return, tax brackets, income tax return, tax refund, taxes, accountant, h&r, tax return calculator, tax forms, free tax filing, federal income tax, federal tax forms, federal tax return, tax online, tax returns, online tax return, irs e file, tax return status, file taxes online, tax preparation, income tax return online, instant tax services, accountants, income tax filing, income tax forms, federal tax, estimate tax return, taxes online, online tax filing, tax services, federal taxes, what is income tax, tax filing, tax questions, online tax, e filing income tax, irs free file, free tax preparation, filing taxes, file taxes, state taxes, tax accountant, h and r, tax planning, free tax return, free federal tax filing, online taxes, free state tax filing, free online tax filing, federal income tax forms, tax help, free tax, how to file taxes, tax preparer, tax consultant, free taxes, income tax returns, complete tax, federal tax forms, free taxes online, income taxes, income tax return efiling, free efile, h&r, tax advisor, tax advice, best place to do taxes in wrentham, wrentham tax, wrentham tax planner, wrentham tax prep, wrentham income, wrentham income tax, wrentham accountant, wrentham accounting