We can help you get the coverage you need – contact us today to get started.

Wrentham, Norfolk, Plainville, Franklin, Walpole, Wrentham insurance, insurance, life insurance, best place for insurance in wrentham, best insurance agency in wrentham, wrentham, LIFE, life insurance awareness month

The sluggish economy continues to put financial strain on many of us. So it just makes sense to examine our budgets and look for ways to trim the fat from our monthly expenses and put more into savings, if possible.

That’s a great way to help stabilize your finances, but it’s also important that you have a financial safety net in place in case something were to happen to you. Life insurance is one of the few guarantees your family could rely on to maintain their quality of life if you were no longer there to provide for them.

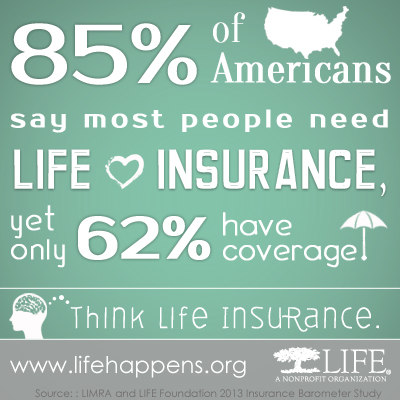

There are 95 million adult Americans without life insurance, according to LIMRA, an insurance industry research group. The fact is, the vast majority of Americans need life insurance and, sadly, most people either have none or not enough. If someone depends on you financially, you need life insurance. It’s that simple.

September is Life Insurance Awareness Month, making it the perfect time to take stock of your life insurance needs. And there are three additional reasons why now is the best time to look into getting life insurance.

You’ll never be younger than you are now. While that may sound obvious, youth is on your side when it comes to life insurance. It makes good financial sense to get coverage when you’re young and healthy, as premiums are based on your age and health. For most policies, your premiums will be locked in at that rate over the life of the policy, and can’t be raised due to a change in your health status.

It’s affordable, with rates near historic lows. People overestimate the cost of life insurance by nearly three times, according to a recent study conducted by LIMRA and the LIFE Foundation, a nonprofit insurance education organization. In fact, life insurance rates remain near historic lows; the cost of basic term life insurance has fallen by nearly 50 percent over the past decade. For example, a healthy 30-year-old can buy a 20-year, $250,000 level-term policy for about $13 per month.

Life happens. One day life is going along smoothly, and the next, you’re thrown a curve ball. No one knows what the future holds. None of us expect to die prematurely, but the truth is roughly 600,000 people die each year in the prime of their lives. That’s why today is always the best day to take care of your life insurance needs.

Life Insurance Awareness Month is the ideal time for a life insurance review. I urge everyone to take a few minutes out of their busy schedules to make sure they have adequate life insurance protection. Consumers can get a general sense of their life insurance needs by going to www.lifehappens.org/lifecalculator and using the online calculator offered by the LIFE Foundation. The next step should be to contact a local insurance professional, who can conduct a more comprehensive needs analysis and help you find the right products to fit your specific needs and budget.

Held each September, Life Insurance Awareness Month is an industry-wide effort that is coordinated by the nonprofit LIFE Foundation. The campaign was created in response to growing concern about the large number of Americans who lack adequate life insurance protection. Roughly 95 million adult Americans have no life insurance, and most with coverage have less than most insurance experts recommend. For more information on life insurance, visit LIFE’s website at www.lifehappens.org.

Call us at 800-560-4637 and we can help you through the entire life insurance process!

Wrentham, Norfolk, Plainville, Franklin, Walpole, Wrentham insurance, insurance, life insurance, best place for insurance in wrentham, best insurance agency in wrentham, wrentham, LIFE, life insurance awareness month

Between mortgages, car loans, credit cards, and student loans, most people are in debt. While being debt-free is a worthwhile goal, most people need to focus on managing their debt first since it’s likely to be there for most of their life.

Handled wisely, that debt won’t be an albatross around your neck. You don’t need to shell out your hard-earned money because of exorbitant interest rates or always feel like you’re on the verge of bankruptcy. You can pay off debt the smart way, while at the same time saving money to pay it off even faster.

Assess the Situation First, assess the depth of your debt. Write it down using pencil and paper or use a spreadsheet like Microsoft Excel. You can also use a bookkeeping program such as Quicken. Include every instance you can think of where a company has given you something in advance of payment, including your mortgage, car payment(s), credit cards, tax liens, student loans, and payments on electronics or other household items through a store.

Record the day the debt began and when it will end (if possible), the interest rate you’re paying, and what your payments typically are. Next, add it all up–as painful as that might be. Try not to be discouraged! Remember, you’re going to break this down into manageable chunks while finding extra money to help pay it down.

Identify High-Cost Debt

Yes, some debts are more expensive than others. Unless you’re getting payday loans (which you shouldn’t be), the worst offenders are probably your credit cards. Here’s how to deal with them.

Don’t use them. Don’t cut them up, but put them in a drawer and only access them in an emergency.

Identify the card with the highest interest and pay off as much as you can every month. Pay minimums on the others. When that one’s paid off, work on the card with the next highest rate.

Don’t close existing cards or open any new ones. It won’t help your credit rating, and in fact, will only hurt it.

Pay on time, absolutely every time. One late payment these days can lower your FICO score.

Go over your credit-card statements with a fine-tooth comb. Are you still being charged for that travel club you’ve never used? Look for line items you don’t need.

Call your credit card companies and ask them nicely if they would lower your interest rates. It does work sometimes!

Save, Save, Save Do whatever you can to retire debt. Consider taking a second job and using that income only for higher payments on your financial obligations. Substitute free family activities for high-cost ones. Sell high-value items that you can live without.

Do Away with Unnecessary Items to Reduce Debt Load Do you really need the 800-channel cable option or that satellite dish on your roof? You’ll be surprised at what you don’t miss. How about magazine subscriptions? They’re not terribly expensive, but every penny counts. It’s nice to have a library of books, but consider visiting the public library or half-price bookstores until your debt is under control.

Never, Ever Miss a Payment Not only are you retiring debt, but you’re also building a stellar credit rating. If you ever move or buy another car, you’ll want to get the lowest rate possible. A blemish-free payment record will help with that. Besides, credit card companies can be quick to raise interest rates because of one late payment. A completely missed one is even more serious.

Pay With Cash To avoid increasing debt load, make it a habit to pay with cash. If you don’t have the cash for it, you probably don’t need it. You’ll feel better about what you do have if you know it’s owned free and clear.

Shop Wisely, and Use the Savings to Pay Down Your Debt If your family is large enough to warrant it, invest $30 or $40 and join a store like Sam’s or Costco–and use it. Shop there first, then at the grocery store. Change brands if you have to and swallow your pride. If you’re concerned about buying organic, rest assured that even at places like Costco you will have many options. Use coupons religiously. Calculate the money you’re saving and slap it on your debt.

Do you plan to donate your services to charity this summer? Will you travel as part of the service? If so, some travel expenses may help lower your taxes when you file your tax return next year. Here are five tax tips you should know if you travel while giving your services to charity.

1. You can’t deduct the value of your services that you give to charity. But you may be able to deduct some out-of-pocket costs you pay to give your services. This can include the cost of travel. All out-of pocket costs must be:

unreimbursed,

directly connected with the services,

expenses you had only because of the services you gave, and

not personal, living or family expenses.

2. Your volunteer work must be for a qualified charity. Most groups other than churches and governments must apply to the IRS to become qualified. Ask the group about its IRS status before you donate. You can also use the Select Check tool on IRS.gov to check the group’s status.

3. Some types of travel do not qualify for a tax deduction. For example, you can’t deduct your costs if a significant part of the trip involves recreation or a vacation. For more on these rules see Publication 526, Charitable Contributions.

4. You can deduct your travel expenses if your work is real and substantial throughout the trip. You can’t deduct expenses if you only have nominal duties or do not have any duties for significant parts of the trip.

5. Deductible travel expenses may include:

air, rail and bus transportation,

car expenses,

lodging costs,

the cost of meals, and

taxi or other transportation costs between the airport or station and your hotel.

For additional help with figuring out you eligible charitable deductions, please contact our office at 800-560-4NFS (4637).

Wrentham, Norfolk, Plainville, Franklin, Walpole, income tax, tax calculator, hr, irs forms, Jackson Hewitt, tax, tax act, tax return, tax brackets, income tax return, tax refund, taxes, accountant, h&r, tax return calculator, tax forms, free tax filing, federal income tax, federal tax forms, federal tax return, tax online, tax returns, online tax return, irs e file, tax return status, file taxes online, tax preparation, income tax return online, instant tax services, accountants, income tax filing, income tax forms, federal tax, estimate tax return, taxes online, online tax filing, tax services, federal taxes, what is income tax, tax filing, tax questions, online tax, e filing income tax, irs free file, free tax preparation, filing taxes, file taxes, state taxes, tax accountant, h and r, tax planning, free tax return, free federal tax filing, online taxes, free state tax filing, free online tax filing, federal income tax forms, tax help, free tax, how to file taxes, tax preparer, tax consultant, free taxes, income tax returns, complete tax, federal tax forms, free taxes online, income taxes, income tax return efiling, free efile, h&r, tax advisor, tax advice, best place to do taxes in wrentham, wrentham tax, wrentham tax planner, wrentham tax prep, wrentham income, wrentham income tax, wrentham accountant, wrentham accounting

By now, you’ve probably heard that this year marks the 80th anniversary of the signing of the Social Security Act. In case you didn’t know, this year is also the 75th anniversary of the payment of the first monthly benefits.

And, today, the Social Security Board of Trustees released the 75th annual report to Congress on the financial status of the Social Security trust funds.

As a quick refresher: The Social Security trust funds include the Old Age and Survivors Insurance (OASI) fund and the Disability Insurance (DI) fund. Benefits to retired workers and their families, and to families of deceased workers, are paid from the OASI trust fund. Benefits to disabled workers and their families are paid from the DI trust fund.

The report shows that, combined, the funds now have an additional year – from 2033 to 2034 – before their reserves are depleted. The Old Age and Survivors fund alone also gets an extra year from 2034 to 2035.

Some factors that led to this improvement include (1) faster growth in average wages in the future, because of slower growth in employees’ private health insurance cost – due at least in part to provisions of the Affordable Care Act, and (2) improvements in how we project the earnings of American workers by age.

The DI fund is still projected to deplete its reserves late in 2016. After that, the income collected through taxes will be enough to pay only 81 percent of the scheduled benefits. So, an adjustment to maintain full disability benefits is needed soon.

The president has proposed temporarily reallocating more of the total Social Security payroll tax rate to the disability fund to give Congress more time to consider comprehensive changes to the Social Security program as a whole.

The Social Security program is sustainable, but needs some adjustments. To keep the program solvent after 2034, Congress could choose to increase payroll taxes by about one-third, reduce benefits by about one-fourth, or make some combination of these or other adjustments.

Because of the importance of Social Security to all Americans, we can be confident that Congress will make timely and well-considered adjustments, just as they have whenever needed since 1935.